October 2023

Normandin Beaudry Pension Plan Financial Position Index on September 30, 2023 – Quebec Municipal and University Sector

Follow this link to consult our index that excludes the Quebec municipal and university sector.

The average pension plan’s going concern position remained relatively stable in Q3 and since the beginning of the year, whereas their solvency position improved during those same periods. Higher interest rates are generally favourable for pension plans, whose financial situation has remained at enviable levels for some quarters.

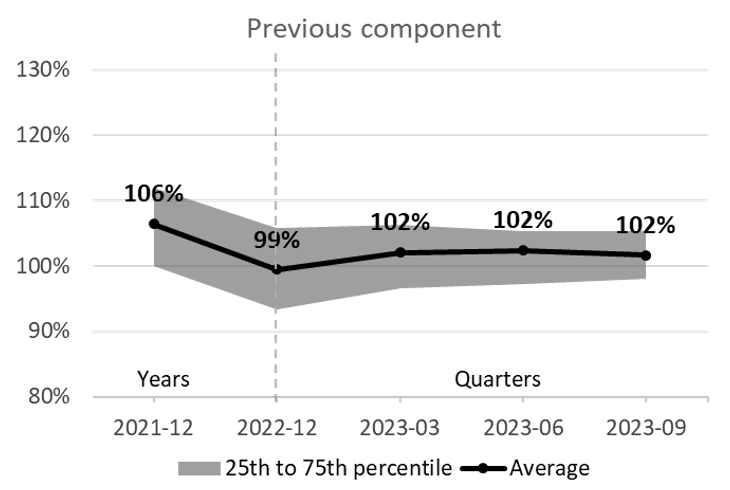

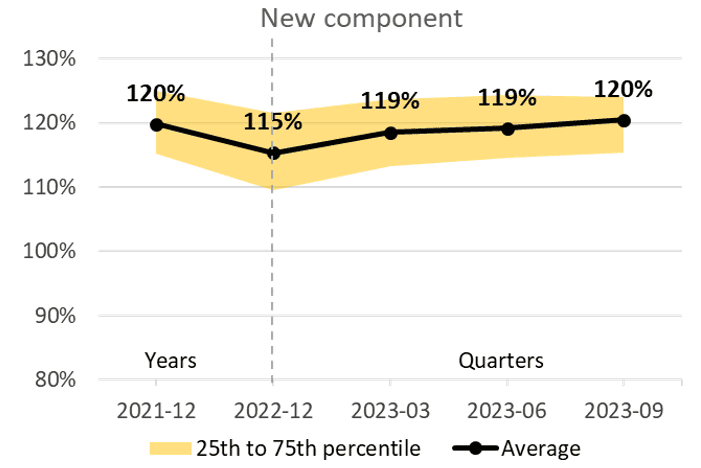

As at September 30, 2023, the average funded ratio of municipal and university sector pension plans is 102% for the Previous component and 120% for the New component (the components distinguish between years of service accumulated before and after January 1, 2014, for the municipal sector and January 1, 2016, for the university sector). The ratio for the Previous component remained stable over the third quarter and is up 3% since the beginning of 2023. The ratio for the Previous component is up 1% over the third quarter and up 5% since the beginning of 2023.

Note: The illustrated funded ratios on a going concern basis are adjusted to include the full market value of the assets, and therefore include the reserve in the Previous component and the stabilization fund in the New component.

The financial position remained relatively stable during the quarter despite volatile financial markets. The markets’ performance was rather poor but was offset by a similar decline in the value of pension plan liabilities. This decline occurred because pension plan liabilities are calculated using higher discount rates following the increase in bond market interest rates.

The rise in discount rates has also brought down current service costs. However, the variation in current service costs will only be reflected at the next actuarial valuation and will depend on the mechanisms in place to stabilize contributions.

The average solvency ratio for municipal and university sector pension plans as at September 30, 2023, is 103% for the Previous component and 114% for the New component. The ratio for the Previous component is up 3% over the third quarter and up 7% since the beginning of 2023. The ratio for the New component remained stable over the third quarter, up 7% since the beginning of 2023.

Higher interest rates have been the key driver of this improvement since the beginning of the year. This is not to mention the effect of the significant rise in interest rates in September, the repercussions of which will be felt in October under the rules set out by the Canadian Institute of Actuaries.

Despite a positive start to the quarter, the average pension fund generated negative returns in Q3 2023 in both stock markets and bond markets. Returns have been generally positive since the beginning of the year, mainly due to positive stock market returns during that period.

Inflation continues to be the focus of attention of various financial markets. Although annual inflation slowed down at the beginning of the year, it remains today above target. The central banks’ battle with inflation is not over, and interest rate hikes may continue for longer than what the markets had initially anticipated. While the economy has proved resilient so far, inflationary pressures may eventually affect the job market and a growing number of companies.

Increases in interest rates over the past two years have resulted in significant decreases in pension plan liabilities, which corresponds to the current value of a pension plan’s future commitments to its members.

If this decline in pension plan liabilities is welcome news from a pension plan’s point of view, can the same be said from the perspective of active members, whose commuted pension values declined at the same pace? Members may only realize the impact of the significant increase in interest rates throughout 2022 when they receive their annual statement this year.

Consider adopting a proactive communication strategy to address this situation. Members’ general meetings are a great opportunity to remind them that, unlike commuted values, the pension accrued in their defined benefit plan is not affected by the ebbs and flows of financial markets.

- Average funding ratio:

- Previous component: 102% as at September 30, 2023 / no change over the quarter and up 3% year-to-date

- New component: 120% as at September 30, 2023 / up 1% over the quarter and up 5% year-to-date

- Average solvency ratio:

- Previous component: 103% as at September 30, 2023 / up 3% over the quarter and up 7% year-to-date

- New component: 114% as at September 30, 2023 / no change over the quarter and up 7% year-to-date

- Negative returns over the quarter in both stock markets and bond markets

- Increase in discount rates on a going concern and on a solvency basis, which decreases the value of liabilities and current service costs

If you have any questions, contact your Normandin Beaudry consultant or email us.

The Normandin Beaudry Pension Plan Financial Position Index is calculated by projecting the pension plan financial data of its clients in the Quebec municipal and university sector. A separate index is published for the plans of Canadian clients outside of this sector. Assets are projected based on the performance of market indices. Liabilities projected on a going concern basis use an estimated discount rate based on each plan’s asset allocation and the sensitivity of asset classes to changes in interest rates on Government of Canada bonds.