July 2023

Normandin Beaudry Pension Plan Financial Position Index on June 30, 2023 – Quebec Municipal and University Sector

Follow this link to consult our index that excludes the Quebec municipal and university sector.

The average pension plan funded ratio changed little in Q2 2023 and year-to-date.

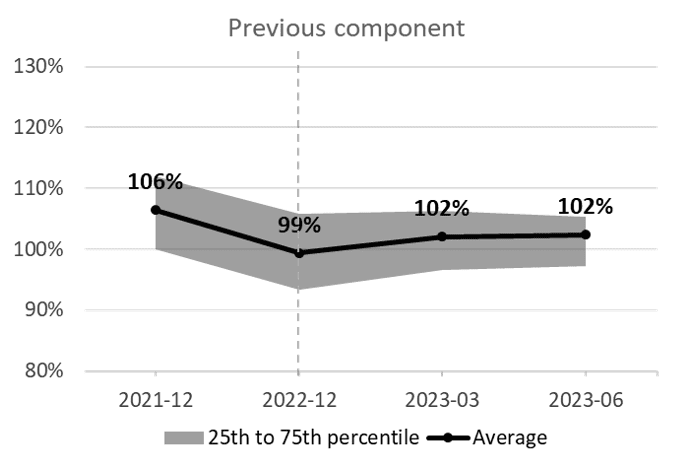

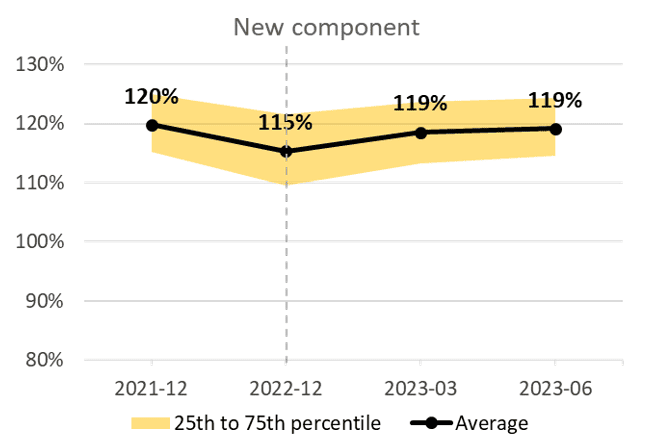

As at June 30, 2023, the average funded ratio of municipal and university sector pension plans is 102% for the Previous component and 119% for the New component (the components distinguish between years of service accumulated before and after January 1, 2014, for the municipal sector and January 1, 2015, for the university sector). The ratios for both plan components are at the same level as at the beginning of the quarter, up 3% and 4% respectively since the beginning of the year.

Note: The illustrated funded ratios on a going concern basis are adjusted to include the full market value of the assets, and therefore include the reserve in the Previous component and the stabilization fund in the New component.

The financial position was little changed in Q2 2023, as investment performance was similar to expected returns and there was no significant change in the discount rates used to value pension plan liabilities.

There was also little change in current service costs in Q2 2023 for the same reason.

The average solvency ratio for municipal and university sector pension plans as at June 30, 2023, is 100% for the Previous component and 114% for the New component. The ratio for the Previous component remained unchanged in the second quarter, but is up 4% since the beginning of 2023. The ratio for the New component is down 2% in the second quarter, but up 7% since the beginning of 2023.

The slight decline in the solvency financial position of the New component in Q2 2023 stems primarily from higher pension plan actuarial liabilities. Despite the slight increase in interest rates in Q2 2023, some discount rates prescribed by the Canadian Institute of Actuaries (CIA) have decreased slightly.

The average pension fund generated slightly positive returns in Q2 2023 and more significant returns since the beginning of the year.

In equity markets, exposure to U.S. equities, especially the technology sector, has been particularly favourable. While the majority of sectors have posted negative or modest returns since the beginning of the year, the seven largest U.S. companies (Apple, Microsoft, Amazon, Nvidia, Alphabet/Google, Tesla and Meta) have generated a return of around 40% since the beginning of the year. Their securities alone explain the overall performance of the U.S. market. The race to develop artificial intelligence is undoubtedly a factor of enthusiasm for this sector.

As for fixed income securities, returns were generally negative during the quarter. The job market turned out to be more resilient than initially anticipated, putting upward pressure on interest rates, especially for bonds with shorter maturities. Credit spreads, which correspond to the additional interest rates offered by the corporate sector relative to federal bond rates, are lower than during the Silicon Valley Bank failure. However, they remain at higher levels than historical averages.

This is the time of year when actuarial valuation results as at December 31, 2022, are produced or are being produced. For some plans, a fully funded Previous component will be welcome news, even though deficit payments resulting from restructuring may continue to be required. As for the New component, a number of plans may be preparing to use surpluses for the first time since the 1990s and may also see a decrease in required current service costs. Surpluses and a decrease in current service costs, although good news, certainly bring challenges and a need for reflection to ensure that the objectives set out in the funding policy are met.

- Average funded ratio:

- Previous component: 102% as at June 30, 2023 / no change over the quarter and up 3% year-to-date

- New component: 119% as at June 30, 2023 / no change over the quarter and up 4% year-to-date

- Average solvency ratio:

- Previous component: 100% as at June 30, 2023 / no change over the quarter and up 4% year-to-date

- New component: 114% as at June 30, 2023 / down 2% over the quarter, but up 7% year-to-date

- Positive equity market returns over the quarter, in particular due to the performance of large U.S. technology companies, and negative returns from fixed income securities

- Little change in discount rates on a going concern basis, so little change in the value of liabilities and current service costs on this basis

- Slight decrease in discount rates on a solvency basis explains the slight pullback in the financial position on this basis for the New component

If you have any questions, contact your Normandin Beaudry consultant or email us.

The Normandin Beaudry Pension Plan Financial Position Index is calculated by projecting the pension plan financial data of its clients in the Quebec municipal and university sector. A separate index is published for the plans of Canadian clients outside of this sector. Assets are projected based on the performance of market indices. Liabilities projected on a going concern basis use an estimated discount rate based on each plan’s asset allocation and the sensitivity of asset classes to changes in interest rates on Government of Canada bonds.